Why is your fund a "fund to watch" and how could it work in an investor's portfolio?

SMD-AM are one of the largest active managers of Japanese equities and we are delighted to make one of our best strategies available to UCITS investors – the SMDAM Japan High Conviction fund.

The fund is managed by Hideyuki TANIUCHI who runs a team that have been running core Japan mandates for the last 23 years, delivering excess returns throughout Japan's value/growth cycles. Following years of successful alpha generation they launched a more concentrated 30 stock portfolio in 2020. The UCITS version of this product was launched in 2024 and is a high conviction core mandate seeking a TOPIX +5% performance target. Since inception it has delivered an annualised excess return of 5.26% with a low tracking error (4.58%) and high information ratio (1.00). The fund has grown to over £100m in the last 9 months given the compelling investment philosophy and alpha potential of the process.

Investing in Japan has long been a challenge for investors. The dispersion in returns between growth and value has presented a factor issue for selectors. By choosing to adopt a core approach to Japan, we believe we can offer a more consistent method of delivering alpha throughout Japan's market cycles.

Can you give an overview of the team running the fund and your investment process?

The portfolio management team responsible for the fund is led by Mr Hideyuki TANIUCHI. He is the lead Portfolio Manager for the High Conviction fund and broader strategy, as well as being the team leader for SMDAM's Market Oriented investment team.

The Market Oriented group has a number of longstanding track records dating back to 2003, and Mr TANIUCHI has over 28 years of investment experience. The team has been managing portfolios according to the process behind the High Conviction fund for over 20 years, and currently they are supported to do so by a 20-strong Tokyo based analyst team and 12 ESG specialists who work with the team on engagement activities and ESG-focused research.

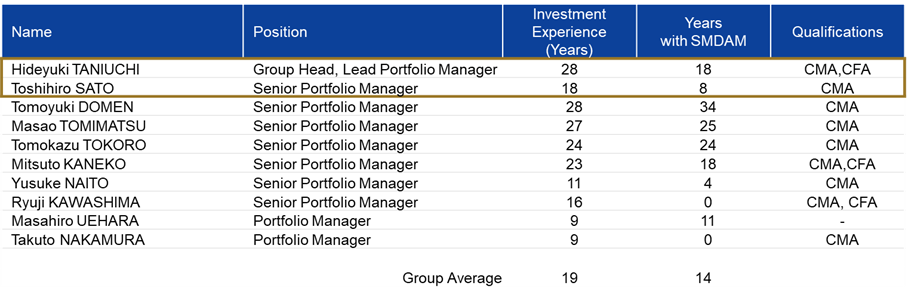

Active debate and interrogation of investment theses is a hallmark of how the team approach manging the portfolio, and the table below summarises the full membership of the Market Orientated Group. All members of the group work within the proposed Japan Equity High Conviction strategy, (strategy inception February 2020), whilst also having additional responsibility for other strategies managed within the group.

What do you see as the key opportunities and risks for your strategy?

The key opportunity for the strategy is undoubtedly the prospect that under Takaichi's leadership the stars can truly align for the Japanese market to deliver excellent performance relative to other developed markets. The positive confluence of corporate governance reform, monetary normalisation, Takaichi's policy agenda and the rotation underway towards industrial sectors Japan has traditionally thrived in potentially sets the stage for years of strong performance. Japan has returned to being unignorable over the past few years as strong performance has driven increased interest. The factors driving this return to relevance have only just started to unfold, and we believe in the years ahead the rewards for the patient reforms build up in Japan over the past decade will fully come to fruition. The greatest risk for our strategy is that exogenous factors intervene to prevent this picture from fully emerging. The primary concerns we have are global instability emanating from further trade disruptions initiated by the Trump administration, or the economic ripple effects from the ongoing conflict in the Middle East. We cannot fully discount the possibility that such supply shocks could bring about a global recession, and were this to happen Japan's exporters would be negatively impacted.

Can you highlight a couple of current investment opportunities within the portfolio (stock, sector or thematic)?

As a high conviction 30-stock portfolio, every name in the fund's portfolio has a strong story behind it and could have been featured here. We have chosen to present the two below due to their connection to currently salient themes.

Yaskawa Electric

It is well-known that Japanese companies hold over half the share in the global robotics market. We like this company because the long-term demand narrative is clearly in favour of their specialised product range. Importantly, Yaskawa Electric is the only major robot maker with a production base in Kyushu, now known as "semiconductor island" where TSMC and other companies have built production facilities. We see the chance for them to leverage this link into large, long-term and high-value orders from semiconductor foundries as extremely exciting.

Toho Co Ltd

A second name that illustrates the diversity of opportunities Japan can produce is Toho. This globally renowned content producer has made steady progress in monetising its unique store of content-based IP. We see a long growth runway ahead for Japan's ability to export their cultural products around the world, and Toho has shown agility and flexibility in how they have hunted down opportunities domestically and outside Japan.