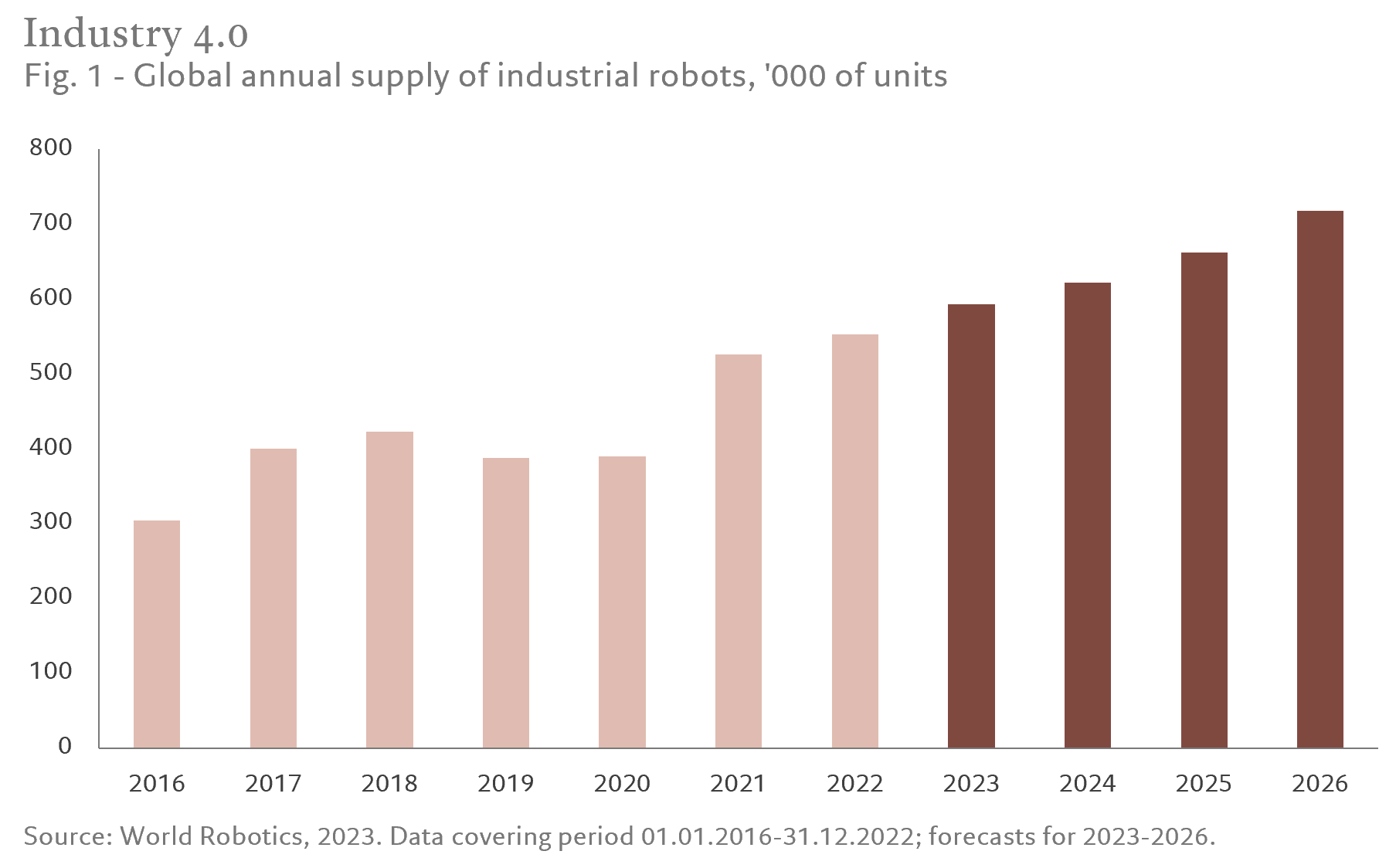

Sixty years ago, the first industrial robot started work in a car assembly line in the US state of New Jersey. Shaped as a giant heavy-lifting arm, it unloaded metal car parts from a die-cast press. Today, robots are no longer confined to the factory floor, they are increasingly part of our day-to-day lives.

There are some 3.5 million of them in the world,1 capable of not only assembling your car but also of hoovering your house, delivering your shopping and even playing bingo with your granny. Yet the signs are the robotics industry has entered a new, more dynamic phase in its evolution.

Advances in technology, be that artificial intelligence (AI) or ever smaller and more powerful semiconductors, are paving the way for the development - and adoption - of a new breed of sophisticated machines. At the same time, labour shortages, an ageing population and falling productivity are fuelling demand for automation.

For investors, this creates a very compelling opportunity, backed by strong secular growth trends and spanning beyond the robots themselves. We see five key themes which will drive the industry over the coming years.

1. Re-shoring and near-shoring

Supply bottlenecks during the Covid pandemic highlighted the dangers of relying on far away countries for manufacturing. Geopolitical tensions between US and China and the war in Ukraine added more pressure on global supply chains. As a result, governments and companies are increasingly looking to shift production to their home territories or at least nearby - so-called "re-shoring" and "near-shoring". This should fuel demand for industrial robots to staff these new factories as well as other automation equipment and software solutions. Some 41 per cent of US manufacturers are looking to increase automation, according to a recent survey by ABB Robotics.2

The semiconductor industry is one of the key sectors targeted by the re-shoring trend, due to the increasingly vital nature of semiconductors and other related technologies, as well as national security concerns. Building semiconductor factories is a major focus of Washington's USD550 billion federal infrastructure spending package, and similar incentives have been approved across several nations and economic unions.

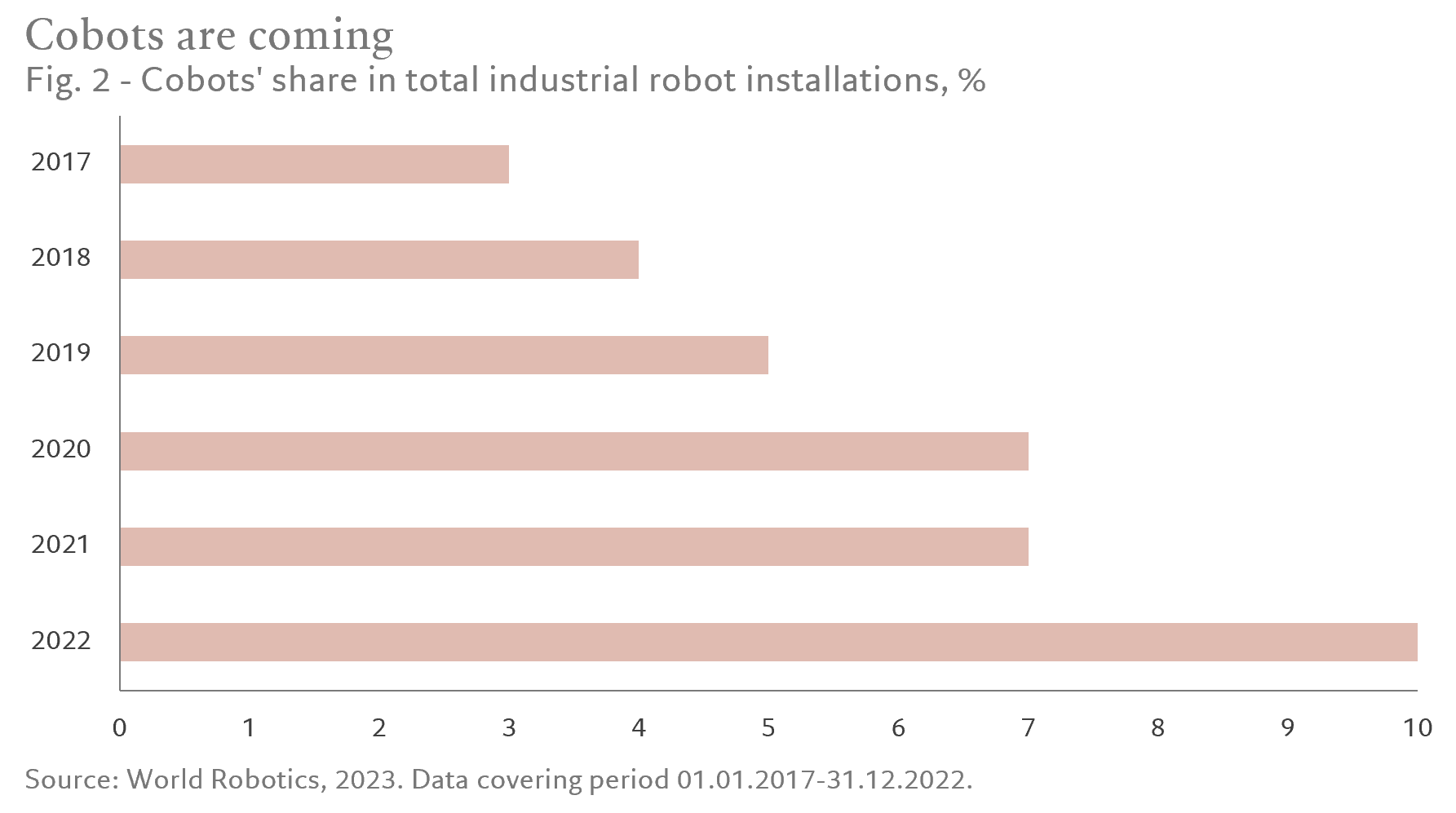

2. Man plus machine: industrial cobots

Assembly-line robots may have long been an industrial staple, but those that work autonomously yet closely in tandem with people are only just beginning to take off. The global cobot market is forecast to reach USD6.8 billion in 2029 from just USD1.2 billion in 2022, which equates to a compound annual growth rate (CAGR) of some 34 per cent.3 We see strong labour shortages, wage inflation, improving and cheaper technology boosting demand for this type of robotic tech. Cobots are proving particularly popular with small and medium sized enterprises (SMEs) and electric vehicle manufacturers, which itself is a major growth area as countries move to outlaw traditional cars to meet net zero targets.

3. Efficiency software

The growth of automation - be that at home or in industry - relies on software. Historically, industrial software, which can be used to operate machines, worked on a buy, install and use forever model. Today, that is increasingly shifting to a software as a service (SaaS) model, through which businesses pay a subscription fee to use the software, with the software itself stored in the cloud, or in a hybrid environment. The industrial software market could more than double to over USD250 billion by 2027, representing a CAGR of 15 per cent.4 This should lead to efficiency gains throughout the process from product design and simulation, to sending the blueprint to the factory or manufacturing partner and optimising the supply chain. Cloud based solutions help reduce the cost and complexities of managing the software itself and also enable data centralisation. Data analytics on top of that is growing strongly as more and more data is generated.5 Business process automation is also growing in popularity, the process through which companies use software solutions to boost the productivity of white collar workers. Furthermore, advances in AI are enabling companies to use large amounts of data to improve operational efficiency.

4. AI and compute

As machines become increasingly sophisticated, they need more processing power to compute and process data. AI is particularly resource intensive, requiring vast amounts of data and processing power to create new content. That means more sophisticated semiconductors. Manufacturers of computing processors appear to be natural beneficiaries of the expansion of AI, but large language models (LLMs) also require other types of chips, such as those that boost memory capacity and bandwidth. Memory, compute and storage semiconductors account for the majority of semiconductor sales. Memory ("DRAM") and storage ("NAND Flash") chips are primarily used for storing data and instructions, while processing chips (such as the core "CPU" in a computer or a complementary accelerator chip like a "GPU") are used for performing calculations and processing data in real time. Also important in the semiconductor food chain are electronic design automation (EDA) companies, like Synopsys, who provide software solutions for the chip designers. The level of innovation and incorporation of AI into the software enable the chip designers to speed up the design phase and improve the power and compute efficiency. Furthermore advances in AI should boost the prospects of semiconductor equipment companies. They provide the chipmaking tools that produce smaller, faster, cheaper, more powerful and energy-efficient microchips. Semiconductor manufacturing plants (known as "fabs") are some of the most highly automated factories in the world, and in turn require increasing usage of AI processes to improve yields and output.

5. Autonomous driving

Robots may have started out making cars, but today they are increasingly driving them. Fully driverless cars, lorries and buses, are still some years away from becoming viable for the mass market. Nevertheless, live trials are already in progress across the world, including in San Francisco, Beijing, Shanghai, and Phoenix. Alphabet-owned Waymo, for example, has notched up millions of miles on public roads (and billions more in simulation), and has been offering driverless rides to San Francisco residents for over a year. Autonomous vehicles are also already partly a reality through the inclusion of various aspects of advanced driver assistance (ADAS) technologies in the latest car models. As these become more common and more advanced, semiconductor demand should surge. By 2031, each car is expected to contain USD1,550 worth of semiconductors, up from just USD665 in 2021, according to research by Gartner.

AI is fuelling a new wave of innovation, revolutionising robotics and automation technologies. Thanks to its ability to increase productivity, reduce costs and help solve the challenges linked to a global labour shortage, we believe robotics and automation is set to grow faster than the broader economy. That creates a very compelling thematic investment opportunity - both in companies that make the robots and in those that provide all the building blocks, from semiconductors to software.

[1] https://ifr.org/ifr-press-releases/news/top-5-robot-trends-2023

[2] https://www.robotics247.com/article/robots_pave_way_reshoring_manufacturing

[3] https://www.marketsandmarkets.com/Market-Reports/collaborative-robot-market-194541294.html

[4] Gartner, 2023

[5] Bank of America and IoT Analytics data, 2021

For more on our approach to Robotics Investing. Click here

This material is for distribution to professional investors only. However it is not intended for distribution to any person or entity who is a citizen or resident of any locality, state, country or other jurisdiction where such distribution, publication, or use would be contrary to law or regulation.

This post is funded by Pictet Asset Management