Highlights

- The Federal Reserve signalled that interest rates could stay higher for longer, which led to volatility in the bond markets in late September.

- Investors should try to see through the volatility and focus on the bigger picture, with markedly improved return forecasts for lower-risk multi-asset portfolios.

- To help investors stay the course, we offer a reminder of how interest rates influence bond returns.

Recent volatility in bond markets in relation to interest rate expectations has presented another test of confidence for multi-asset investors, particularly those clients invested in lower-risk, high bond allocation portfolios. But the higher-for-longer interest rate outlook is a major reason multi-asset investors should hold their nerve amid the turbulence.

Yields on 10-year government debt in the US, euro area and UK rose (reflecting a drop in prices) following central bank policy meetings and key inflation data releases in late September, namely comments from the US Federal Reserve (Fed) and Bank of England (BoE) that suggested interest rates may not come down as soon as markets were expecting.

It all comes down to the influence of interest rate expectations—and how they change—on bond returns. Given the consensus that rates are close to or at peak levels and the market's sensitivity to changes in the outlook for rates, now is as good a time as ever to explore the role of interest rate expectations in bond market returns.

Why have bond markets been volatile?

Recent bond market volatility came in the wake of comments by Fed and BoE policymakers at their September policy meetings, which came as a surprise for markets. The market consensus at the time was that interest rates would start falling in early 2024.

Interest rate expectations are a key factor in bond prices, so understanding how bond markets tend to move in response to interest rates can help investors make sense of market turbulence and ultimately focus on the long term.

Why interest rates influence bond prices

An increase in interest rates pushes the price of existing bonds down, while falling rates would typically see long-term bond prices rise. This repricing of bonds is based on the return an investor would receive if they held the bond to maturity (yield-to-maturity). If rates are going up, existing bond prices tend to fall because investors can earn more on newer bonds with higher coupons, so the price of existing bonds typically drops, giving investors an incentive to buy those bonds. The opposite is true when rates are falling.

In the case of government bonds, expectations about future interest rates can have an even bigger impact on bond prices than actual movements in rates. This is because when the policy rate, set by central banks, is expected to rise or fall in the future, parts of the market will adjust their bond holdings to optimise returns, which can see prices move further based on increased demand.

For example, if investors expect interest rates to fall from current levels, there tends to be increased demand for longer-term bonds as these will yield a higher return over time than shorter-term bonds. On the other hand, if markets expect interest rates to rise, then short-term bonds become more attractive as they are less sensitive to interest rate changes.

Sensitivity to interest rate changes is referred to as duration risk, which is measured in years and considers a bond's characteristics, such as yield, coupon rate and maturity. We explain duration risk—and its role in the unprecedented 2022 bond market sell-off—in more depth here.

While it might sound like a simple relationship that investors can exploit to their advantage, markets—including many professional investors—can get it wrong. If interest rates don't move as expected, investors that have taken a tactical position with their bond holdings could suffer far greater losses than a bond portfolio that is diversified across the yield curve.

Even if interest rates do move as expected, the yield curve, which tracks yields across the spectrum of bond maturities, doesn't always move in parallel, i.e., parts of the curve may move more than other parts of the curve, and so taking concentrated positions at any point along the yield curve incurs a high level of risk.

Ultimately, bond holdings have historically offered a counterbalance to the volatility in equity markets1, so it's important that multi-asset investors think very carefully before introducing further risk to their bond exposures.

Why multi-asset investors should hold their nerve

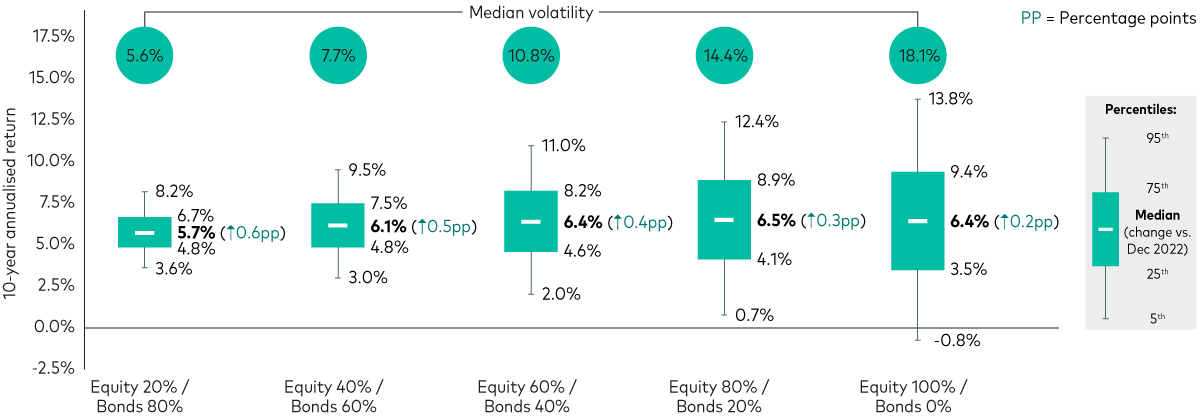

While the higher-for-longer message from US and UK policymakers in September shattered the market consensus that rate cuts would come in early 2024, multi-asset investors shouldn't lose sight of the bigger picture - that the aggressive rate-hiking programme by major central banks in the past 18 months has markedly improved our long-term return outlook for bond investors, thanks to greater income returns going forward.

The chart below shows our average annual return expectation for sterling investors across different equity/bond splits. The numbers in brackets show the improvement in our median return expectation between 31 December 2022 and 30 June 2023, with lower-risk, higher bond allocation portfolios seeing the greatest uplift in expected returns.

Long-term multi-asset portfolio return forecasts

Lower-risk portfolios benefit more from rate rises

Any projections should be regarded as hypothetical in nature and do not reflect or guarantee future results.

Source: Vanguard calculations in GBP, as at 30 June 2023 median numbers in brackets as at 31 December 2022.

Notes: The forecast corresponds to the median of 10,000 VCMM simulations for 10-year annualised nominal returns in GBP for multi-asset portfolios highlighted here. Asset-class returns do not take into account management fees and expenses, nor do they reflect the effect of taxes. Returns do reflect the reinvestment of income and capital gains. Indices are unmanaged; therefore, direct investment is not possible. Equity comprises UK equities and global ex-UK equities. Fixed income comprises UK bonds and global bonds ex-UK (hedged). UK equity home bias: 25%, UK fixed income home bias: 35%. Indices used for benchmarks: UK equities = MSCI UK Total Return Index; global ex-UK equities = MSCI AC World Total Return Index; UK bonds = Bloomberg Sterling Aggregate Bond Index; global bonds ex-UK (hedged) = Bloomberg Global Aggregate ex Sterling Bond Index Sterling Hedged.

IMPORTANT: The projections and other information generated by the VCMM regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results and are not guarantees of future results. Distribution of return outcomes from VCMM are derived from 10,000 simulations for each modelled asset class. Simulations are as at 31 December 2022 and 30 June 2023. Results from the model may vary with each use and over time.

The key message for multi-asset investors, particularly those with a preference for lower risk, is that we are most likely at or close to peak rates across key markets and the long-term outlook has improved for bond investors. While rates may not come down as soon as markets had anticipated, if and when they do trend down, we would expect to see long-term bond prices rise.

The difficulty of trying to position portfolios tactically is why maintaining a globally diversified exposure to markets is a prudent investment strategy. Where we are in the current interest rate cycle offers further reason to ensure client portfolios include a diversified exposure to global bond markets that aligns with their long-term goals and preferences around risk.

Model Portfolio Solutions at Vanguard

Our Model Portfolio Solutions (MPS) combine all the features of Vanguard's top-selling multi-asset funds within the model portfolio format, giving advisers more ways to deliver value through low-cost, ready-made portfolio solutions.

1 Vanguard analysis based on Bloomberg data. Analysis of annual total return of global equities and global bonds between 29 December 2001 and 31 December 2022 found that global bonds delivered a positive return in five of the six years that global equity markets posted losses. Bonds: Bloomberg Global Aggregate Total Return index (hedged in GBP); Shares: FTSE All-World Total Return index (in GBP). The performance of an index is not the exact representation of any particular investment. As you cannot invest directly into an index, the performance does not include the costs of investing in the relevant index. Basis of performance NAV to NAV with gross income reinvested.

Investment risk information

The value of investments, and the income from them, may fall or rise and investors may get back less than they invested.

Any projections should be regarded as hypothetical in nature and do not reflect or guarantee future results.

Funds investing in fixed interest securities carry the risk of default on repayment and erosion of the capital value of your investment and the level of income may fluctuate. Movements in interest rates are likely to affect the capital value of fixed interest securities. Corporate bonds may provide higher yields but as such may carry greater credit risk increasing the risk of default on repayment and erosion of the capital value of your investment. The level of income may fluctuate and movements in interest rates are likely to affect the capital value of bonds.

IMPORTANT: The projections or other information generated by the Vanguard Capital Markets Model® regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. VCMM results will vary with each use and over time. The VCMM projections are based on a statistical analysis of historical data. Future returns may behave differently from the historical patterns captured in the VCMM. More important, the VCMM may be underestimating extreme negative scenarios unobserved in the historical period on which the model estimation is based.

The Vanguard Capital Markets Model® is a proprietary financial simulation tool developed and maintained by Vanguard's primary investment research and advice teams. The model forecasts distributions of future returns for a wide array of broad asset classes. Those asset classes include US and international equity markets, several maturities of the U.S. Treasury and corporate fixed income markets, international fixed income markets, US money markets, commodities, and certain alternative investment strategies. The theoretical and empirical foundation for the Vanguard Cahpital Markets Model is that the returns of various asset classes reflect the compensation investors require for bearing different types of systematic risk (beta). At the core of the model are estimates of the dynamic statistical relationship between risk factors and asset returns, obtained from statistical analysis based on available monthly financial and economic data from as early as 1960. Using a system of estimated equations, the model then applies a Monte Carlo simulation method to project the estimated interrelationships among risk factors and asset classes as well as uncertainty and randomness over time. The model generates a large set of simulated outcomes for each asset class over several time horizons. Forecasts are obtained by computing measures of central tendency in these simulations. Results produced by the tool will vary with each use and over time.

Important information

For professional investors only (as defined under the MiFID II Directive) investing for their own account (including management companies (fund of funds) and professional clients investing on behalf of their discretionary clients). In Switzerland for professional investors only. Not to be distributed to the public.

The information contained in this document is not to be regarded as an offer to buy or sell or the solicitation of any offer to buy or sell securities in any jurisdiction where such an offer or solicitation is against the law, or to anyone to whom it is unlawful to make such an offer or solicitation, or if the person making the offer or solicitation is not qualified to do so. The information in this document does not constitute legal, tax, or investment advice. You must not, therefore, rely on the content of this document when making any investment decisions.

The information contained in this document is for educational purposes only and is not a recommendation or solicitation to buy or sell investments.

Issued in EEA by Vanguard Group (Ireland) Limited which is regulated in Ireland by the Central Bank of Ireland.

Issued in Switzerland by Vanguard Investments Switzerland GmbH.

Issued by Vanguard Asset Management, Limited which is authorised and regulated in the UK by the Financial Conduct Authority.

© 2023 Vanguard Group (Ireland) Limited. All rights reserved.

© 2023 Vanguard Investments Switzerland GmbH. All rights reserved.

© 2023 Vanguard Asset Management, Limited. All rights reserved.