For the first in a long time, 2017 saw a resurgence in global earnings growth. Fidelity Global Special Situations Fund Manager Jeremy Podger assesses whether this dynamic can continue to support markets and the potential implications for market leadership in the coming months.

Key points

- After years of stagnant earnings, 2017 saw an improving picture as global earnings growth broadly kept up with the rise in markets.

- With economic indicators generally very positive and supportive of corporate earnings, we could now be in a new "earnings driven" phase of market growth.

- While the US will benefit from tax reform in this regard, there are arguably more attractive opportunities in Europe and Japan at this stage of the cycle.

After years of stagnant earnings growth (in US dollar terms), the rate of global earnings growth in 2017 was broadly similar to the rise in markets. Given this, we could say that we appear to have moved from a "revaluation" phase to a new "earnings driven" phase of market growth.

At the end of last year, the consensus view was looking for US earnings to grow a further 12.6% in 2018. However, the passage of the tax reform bill, which was not in these estimates at the time, could propel US earnings growth into the teens (in % terms) this year. There may be scope to surprise positively outside the US as well.

So this should be supportive of markets this year, although one should note that growth in 2018 (and then 2019) is unlikely to be up to last year's strong showing. Against that is the expectation of a tightening of liquidity conditions with further rate rises in the US and some "tapering" of quantitative easing in Europe. Meanwhile economic indicators are generally very positive (though admittedly one could worry they cannot get much better).

Overall at this stage my working assumption is that the current benign economic backdrop is most likely to lead to investors focusing more outside the US now that earnings growth has reappeared and valuations are relatively more favourable.

Trailing P/E ratios

Source: Fidelity International, Bloomberg, 31 December 2017.

Source: Fidelity International, Bloomberg, 31 December 2017.Whilst the central case may be that the rest of the world now outpaces the US which is more expensive (even after tax reform), more mature in terms of the profit cycle and where companies have generally taken on more debt (unlike elsewhere in the world), if there is some kind of crisis, the US would be expected to exhibit more defensive qualities as it has done in the past. A sharp sell-off could be caused by any of a number of possible geopolitical events - one example might be an oil price related inflationary shock.

In the absence of such an unforeseeable shock, it is reasonable to expect the US market to correct if and when monetary conditions are significantly tightened and earnings growth turns negative. This will happen at some point but appears less likely on a 12-month view.

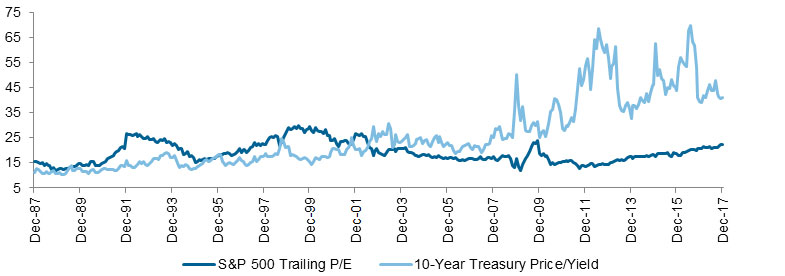

Looking at market levels, it is difficult to deny that low bond yields have had some influence in dragging up equity market valuations in recent years. The chart below shows the US equity Price/Earnings (PE) ratio compared to the "PE" of bonds (the inverse of the yield) since 1970. Whilst investor sentiment in the US amongst private investors is very positive currently (though less so amongst professional investors), we see that actual fund flows in the US have been more directed to bonds than equities since the financial crisis.

S&P 500 Trailing P/E vs 10-Year Treasury Price/Yield

Source: Fidelity International, Bloomberg, Bank of America Merrill Lynch, 31 December 2017.

Source: Fidelity International, Bloomberg, Bank of America Merrill Lynch, 31 December 2017.There has been a similar picture for other regions, suggesting it is at least possible that with fixed income yield spreads now very compressed, investors could deploy more risk capital into equities in general in the coming year. Thus, at this stage I am inclined to be generally positively disposed towards European, Japanese (seeing very strong earnings growth currently) and other Asian markets and a little more cautious on the US, despite the recent boost from tax reform.

As an aside, technology has far outstripped all other sectors in performance terms last year. This largely reflects some very powerful earnings growth so that earnings/cash flow-based valuations (relative to the broader market) are generally currently below long-term averages. This does not mean, however, that many of the better performing names may not correct somewhat when the recent rapid growth inevitably slows down and the high profile mega-cap names are surely vulnerable in this regard.

In conclusion, in my opinion, subject as ever to unforeseen events, equities remain well supported. The focus, in the year ahead, remains on finding the best stock opportunities for our investors globally.

Important information

The value of investments and the income from them can go down as well as up, so you may not get back what you invest. Past performance is not a reliable indicator of future returns. Investors should note that the views expressed may no longer be current and may have already been acted upon. The Fidelity Global Special Situations Fund uses financial derivative instruments for investment purposes, which may expose it to a higher degree of risk and can cause investments to experience larger than average price fluctuations. Changes in currency exchange rates may affect the value of an investment in overseas markets. Investments in small and emerging markets can also be more volatile than other more developed markets. The value of bonds is influenced by movements in interest rates and bond yields. If interest rates and so bond yields rise, bond prices tend to fall, and vice versa. The price of bonds with a longer lifetime until maturity is generally more sensitive to interest rate movements than those with a shorter lifetime to maturity. The risk of default is based on the issuer's ability to make interest payments and to repay the loan at maturity. Default risk may therefore vary between different government issuers as well as between different corporate issuers. Reference in this document to specific securities should not be interpreted as a recommendation to buy or sell these securities, but is included for the purposes of illustration only.

Related funds

FID FIF - Fidelity Global Special Situations Fund W-ACC-GBP

Fund profile

Quarterly performance review (PDF)

Jeremy Podger joined Fidelity in February 2012 and manages the Fidelity Global Special Situations Fund and the Fidelity World Fund (SICAV). He is an experienced investor and has been managing global equities mandates for more than 20 years. Prior to Fidelity, Jeremy was Head of Global Equities at Threadneedle, a fund manager at Investec for seven years and a global and pan-European fund manager for Saudi International Bank. Jeremy has a degree from Cambridge University and an MBA from London Business School.